On July 29 at the Sunnyvale Tech Corner Campus in Calif., Google hosted the open source community for the inaugural CORD Summit. CORD, or Central Office Re-architected as a Datacenter, launched last week as an independently funded On.Lab software project hosted by The Linux Foundation. The sold-out event featured interactive talks from partners and leading stakeholders of the newly formed CORD Project, including AT&T, China Unicom, Ciena, Google, NEC, ON.Lab, ONF, The Linux Foundation, University of Arizona, and Verizon.

CORD is the biggest innovation in the access market since ADSL and the cable modem. Considering the broad scope of the access network, and the technical roadmap the growing open source CORD community laid out at the Summit, CORD has the potential to redefine the economics of access.

To understand the importance of CORD we must first understand how a Tier 1 network is constructed. We’ve all seen network diagrams on whiteboards or PowerPoint slides illustrating routers, switches and optical transport equipment with rectangles or circles connected by straight lines, rings, or perhaps a Cloud. An often overlooked aspect is that these pieces of metal must reside in a physical building. On one side, “the Cloud” represents Cloud companies like Google and Amazon, Over-the-Top Providers (e.g., Netflix) and the Service Providers’ (SP’s) own Cloud infrastructure. On the other side is “Access.” To get from your home or building to “the Cloud,” your packets must first go through customer premise equipment (CPE) provided by the SP, followed by the outside plant (OSP), the local central office (CO), the metro CO and then the large city CO where the large SP’s interconnect or peer with other SPs and the Cloud companies.

The Cloud datacenter (DC) has experienced an innovation boom driven by the massive increase in Cloud computing and “big data.” Modern datacenters are pristine with raised flooring, state-of-the-art HVAC systems, and hot and cold aisles. COs are not pristine. They are, however, strategically located in downtown locations in every city and town in your country. COs can usually be identified as the building near the center of town with few, if any, windows. The local CO is just the beginning of the access, or broadband, network. The end is in a box (CPE), such as an ONT/ONU, Cable Modem, or Gateway, in every home and building the SP serves.

This access network, or “last mile,” is a challenging business. The network encompasses thousands of miles of facilities (wires) that radiate from COs and cable hubs, and terminate in nearly every home and building in the serving area. It includes specialized outside plant electronics deployed in cabinets, underground vaults and mounted to utility poles. Onerous federal, state and local regulations that hinder flexibility add to the challenges, as well as real operational setbacks such as lightning strikes, floods, backhoe fades and squirrel chews.

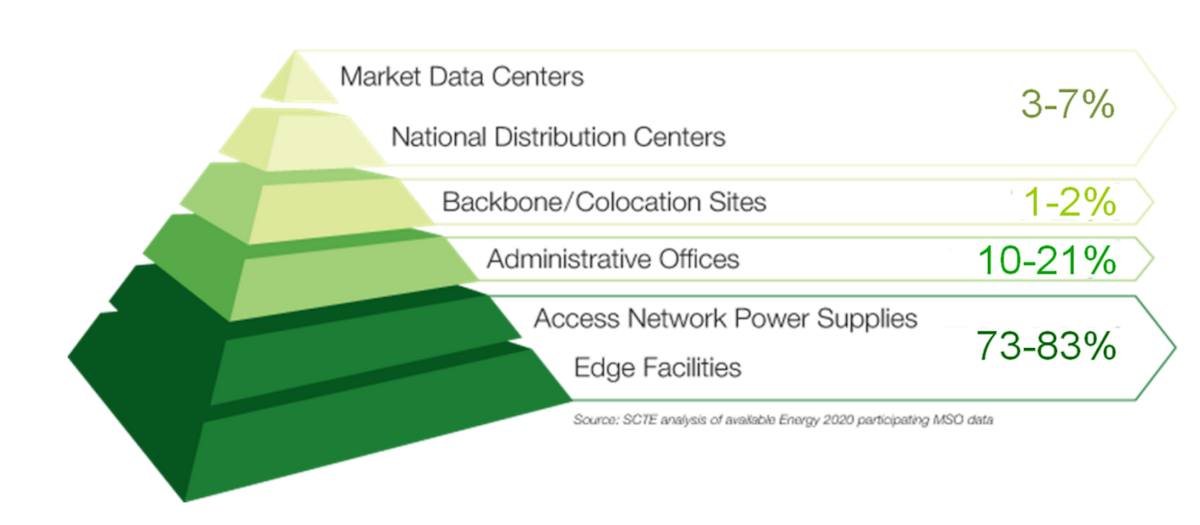

An important consideration for understanding the value of CORD is the economic scope of the CO and access network. The modern DC can consume 100’s of megawatts of electricity. For SPs, these are few and far between.For example, Comcast only has three large DCs. Big city CO’s would encompass perhaps the largest 50 cities in the USA with the medium city CO’s covering a few hundred more. However, in the USA, close to 20,000 local COs connect 10’s of thousands of endpoints (buildings); AT&T owns 4,700. Many of these facilities are “unmanned.” To illustrate this scope, the SCTE’s Energy 2020 program produced the “Energy Pyramid,” showing that 73-83% of a cable company’s energy bill goes to the access network. Given that Comcast’s electric bill is over $1 billion, the access network consumes real money. And don’t forget the fleet of bucket trucks that are an integral part of the access network.

The large number of CO’s are only the beginning of the CORD challenge. In the USA, COs are more than 50 years old, with many decades older. They have evolved over time, from early analog voice switches, to the Class 5 PSTN switch, to Frame Relay, ISDN, digital loop carriers, ADSL, DOCSIS, GPON, and so on. During this period, the racks and bays of installed base of equipment was simply added onto with other proprietary purpose-built hardware devices. This resulted in a conglomeration of technologies located where convenient during the time of installation. This led to more than 300 different types of equipment from dozens of vendors each with their own management system, leading to enormous operational expenses (OPEX). Capital expenses (CAPEX) are a one-time event with a 5 to 7 year depreciation cycle. OPEX, on the other hand, remain ongoing as long as the equipment is in operation. It’s no surprise that adding a new service to this mix is an expensive and time-consuming challenge.

Keep in mind the SP’s design for “5 Nines” (99.999% uptime) availability. The access network can only be down 4.7 minutes per year. A reboot may only take 5 minutes, but that’s over the SP’s budget for the year. If the closest replacement part (sparing) is 20 minutes away in the regional warehouse, the SP could get fined by the FCC, (E911 is serious business). The alternative is to stock 300 different spares in every CO (with secondary spares in the regional warehouse). The resulting purchasing and logistic systems add to the high OPEX and limit flexibility.

CORD must address the above real-world, street-level challenges. Specific to the access or broadband network are the current access equipment architectures. SP’s look to virtualization for more than “cheap” hardware. They must adapt their business models to better compete with the deep-pocketed, aggressive cloud companies who want them to become the proverbial dumb pipe.

One of the many desired outcomes of virtualization is to better align expenses with actual demand.Consider a GPON network. Located in the CO is the Optical Line Terminal (OLT). These are expensive, proprietary and large chassis devices that can support upwards of 5,000 homes with a 1:32 split, (32 homes per port). What if you have 5,010 subscribers? You must purchase and install a second large chassis and only populate a few slots. Thus, while demand may be growing linearly or exponentially, your capacity can only grow in a large step function.

CORD is an ambitious project that addresses the most difficult and economically challenging part of any SP’s network: The Access Network or Last Mile. With the move to more and more gigabit cities, a linear extension of today’s technologies and architectures is unsustainable. The bar is high, but as shown in Sunnyvale last week, the CORD community is ripe for the challenge.

{kind=link}